Oil Prices Rise on Tight Summer Market

Oil demand is not going away, and that is The Crude Truth

As we navigate the peak of summer 2025, oil markets are heating up—literally and figuratively. Brent crude futures have climbed above $70 per barrel, driven by a combination of dwindling U.S. inventories, robust seasonal demand, and escalating geopolitical tensions.

This surge highlights the fragility of global energy balances during periods of high consumption, reminding us that even in an era of transitioning energy sources, oil remains the dominant force for now.EIA's Latest Insights: Inventory Draws and Demand Surge

The U.S. Energy Information Administration (EIA) released its Weekly Petroleum Status Report on July 16, 2025, for the week ending July 11, revealing a significant drawdown in crude oil inventories.

Commercial crude stocks fell by 3.9 million barrels to 422.2 million barrels, marking a stark 8% below the five-year average for this time of year.

This draw exceeds analyst expectations of a modest 552,000-barrel decline, highlighting tighter-than-anticipated supplies amid the summer driving season.

Notably, this comes after adjustments in prior weeks' data. For instance, the week ending July 4 saw an unexpected build of 7.1 million barrels, revised slightly in subsequent reports, while the July 2 week reported a 3.8 million-barrel increase.

These fluctuations reflect ongoing refinements in EIA's methodology, including better accounting for imports, exports, and refinery runs. Crude imports rose by 366,000 barrels per day to 6.4 million bpd, while exports jumped 761,000 bpd to 3.5 million bpd in the latest week, signaling dynamic trade flows.

On the demand front, the EIA anticipates a modest uptick in U.S. oil consumption for 2025, rising to 20.4 million barrels per day from 20.3 million in 2024, with steady levels projected into 2026.

Summer 2025 is proving particularly robust, with gasoline demand spiking due to holiday travel and economic recovery. The International Energy Agency (IEA) echoes this, noting healthy refinery margins and a tighter physical market than implied by Q2 stock builds of 1.74 million bpd.

Despite builds in gasoline stocks (up 3.4 million barrels last week), overall fuel inventories are offsetting only part of the demand pressure, keeping prices elevated.

Geopolitical risks are amplifying these fundamentals. Recent drone attacks on oilfields in Kurdistan have curtailed output by about 200,000 bpd, while Israeli military actions in Syria add to regional instability.

Combined with uncertainties over U.S. tariffs and global growth, these factors contribute to near-term volatility.

Market Outlook: Tight Now, Looser Later?

Analysts like those at Morgan Stanley maintain a Brent outlook of $65 by year-end, expecting prices to soften as summer demand wanes and inventories potentially rebuild.

However, the IEA warns of steep backwardation in prompt time spreads, indicating immediate tightness that could persist if supply disruptions continue. For now, the market's backwardation—where near-term contracts trade at a premium—signals bullish sentiment for the short haul.

Investor Considerations: Navigating Oil and Gas Opportunities

With oil prices responding to these dynamics, investors eyeing the sector should adopt a nuanced approach, balancing short-term gains with long-term risks. Here's what to watch for in both publicly traded and privately held oil and gas investments.

Publicly Traded Companies

Public oil and gas firms, such as majors like ExxonMobil or independents like Occidental Petroleum, offer liquidity and exposure to price swings. Key factors to evaluate include:

Production Costs and Efficiency: Look for companies with low breakeven prices (ideally under $50 per barrel) to weather downturns. Firms leveraging technology for enhanced recovery in shale plays, like the Permian Basin, are resilient.

Balance Sheet Strength: Prioritize those with low debt-to-equity ratios and strong cash flows. Dividend yields are attractive—many yield 4-6%—but check payout sustainability amid volatility.

ESG and Diversification: Increasingly, investors demand environmental, social, and governance (ESG) compliance. Companies investing in carbon capture or renewables hybrids may command premiums.

Macro Indicators: Monitor EIA forecasts for U.S. production, expected to average 13.4 million bpd in 2025 and 2026, down slightly from peaks due to maturing fields.

Geopolitical premiums could boost short-term returns, but watch for oversupply risks from non-OPEC sources.

Volatility is inherent; consider ETFs like the United States Oil Fund (USO) for broad exposure without picking individual stocks.

Privately Held Companies with Tax Advantages

For accredited investors, private oil and gas ventures—often through direct participation programs (DPPs) or limited partnerships—provide unique tax benefits under U.S. tax code Sections 263 and 611. These include intangible drilling costs (IDCs) deductions (up to 100% in the first year) and depletion allowances (15% of gross income tax-free).

What to look for:

Reserve Quality and Operator Expertise: Scrutinize proven reserves via independent audits. Experienced operators in prolific basins reduce dry-hole risks.

Tax Efficiency and Returns: These investments can offset ordinary income, ideal for high earners. Aim for internal rates of return (IRRs) of 15-25%, but factor in illiquidity (hold periods of 5-10 years).

Risk Mitigation: Diversify across wells or funds. Regulatory compliance is key—ensure adherence to SEC rules for private placements.

Market Alignment: With EIA projecting steady demand growth, focus on upstream assets poised for summer peaks. However, energy transition risks loom; seek ventures with methane reduction tech for longevity.

In both arenas, due diligence is paramount. Consult financial advisors, as oil's cyclical nature demands patience. While the tight summer market offers upside, positioning for a balanced energy future will define long-term success.

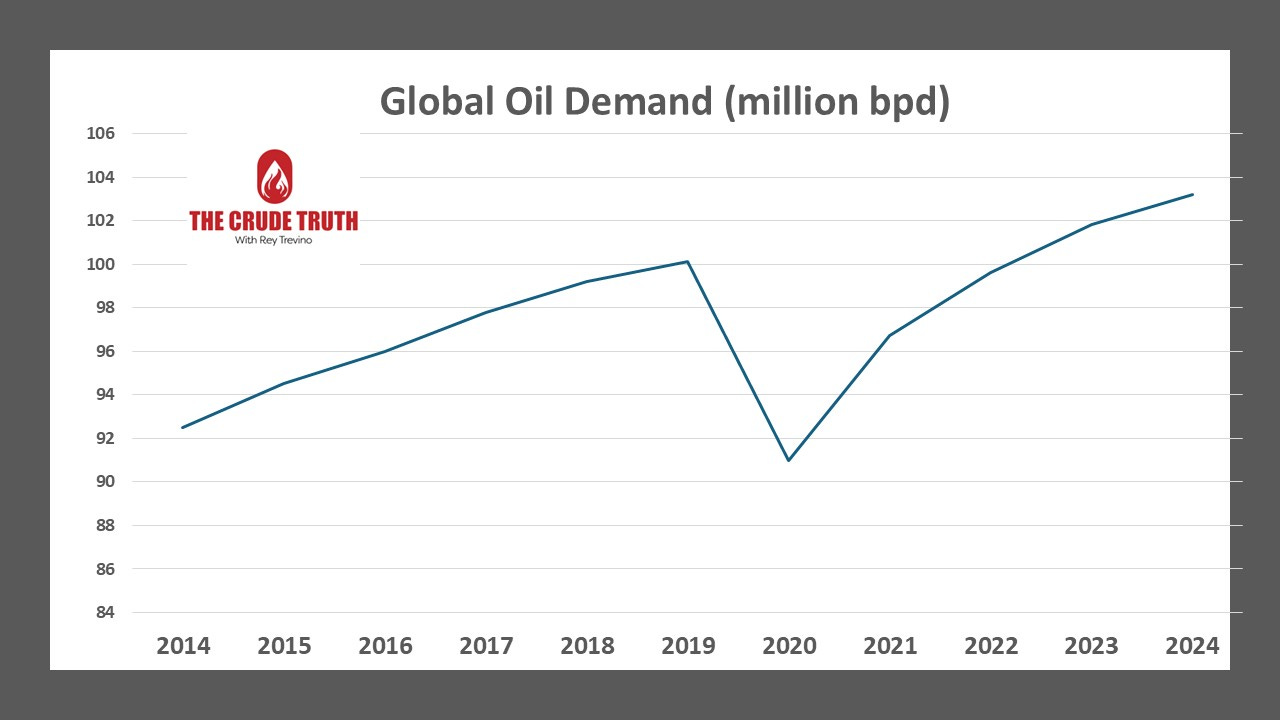

With all of the demand numbers coming out showing that we will have hit another year of peak demand and production, and renewable energy globally has spent trillions of dollars, and only lowered fossil fuel input on the grid by 2%, oil and gas will be needed for several decades. Until we get a breakthrough in technology, the demand will remain stronger than ever due to the failure of wind and solar to deliver on their promises of “Cheap renewable” energy.

Still a long-term oil bull, and that is The Crude Truth.

I am currently working on a series of articles on how Oil and Gas compares to Real Estate as investments. There have been numerous requests for information, and we need to help share what we have found.